An article by

Andreas Wegmann

Published on

03/12/2024

Updated on

03/12/2024

Reading time

5 min

The global card industry will certainly not go under any time soon, but at least in the Euro countries it will lose business from 2025. SEPA Instant Payments (SCT Inst) will be able to replace card payments in many cases. The article explains why this is the case.

Cashless Payment with Card or Smartphone

Fewer and fewer people care about cash and instead want to pay everywhere with a card (or their smartphone, where the card details are stored). The infrastructure required for this is difficult to understand because there are national (in Germany the girocard) and some international card systems (best known are Visa and Mastercard). What all card systems have in common is that the cardholder does not pay any fees for purchases, but rather receives additional benefits (discount points, insurance benefits, lottery tickets, …).

The so-called acceptance point (retailer, travel agency, restaurant, petrol station, …) is charged a share of the turnover (merchant service charge) and this money is used to finance the entire card system. In international business, income is still generated through currency exchange (but the credit interest on the “credit cards” ends up with the bank and not the card company).

A glance at the balance sheets of the major card companies is enough to realise that this is a multi-billion Euro business with high returns. On the flip side of this coin is the burden this system places on national economies, as the cost of payment ultimately results in higher prices.

The Core of the Problem: the Card Terminal

At the point of sale (POS), there is a card terminal that records the customer’s card data and transmits it to the authorisation system to get a confirmation for the transaction.

At the point of sale (POS), there is a card terminal that records the customer’s card data and transmits it to the authorisation system to get a confirmation for the transaction.

While the theft of a single card can cause manageable damage to the system, a card terminal comes into contact with many hundreds of card data. The card terminal is therefore a major risk factor in the payment process. Over the years, driven by fraud, these terminals have become increasingly secure (e.g. via chip & PIN procedure) and therefore more complex.

The necessary transmission paths (network operation) to the authorisation system and the authorisation system itself must also meet the highest security standards and be constantly upgraded.

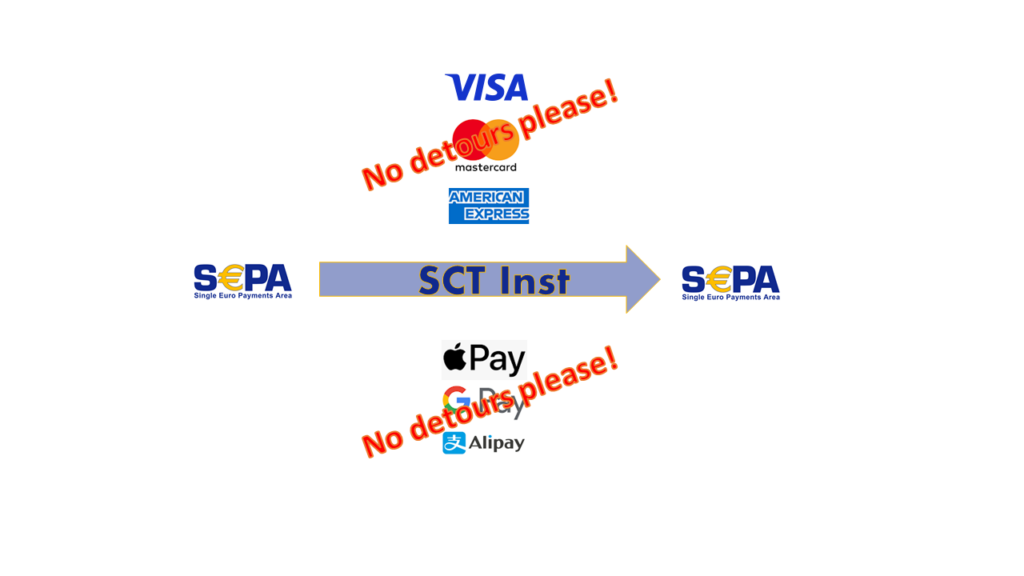

SCT Inst at POS

SCT Inst transactions are sufficiently fast to be used at the POS for many applications. However, the most important advantage of SCT Inst at the POS is that this type of transaction works completely differently and does not require a separate authorisation system. The merchant does not need a card terminal, but only has to transmit his (!) data to the buyer. This means that there is no longer a device at the POS that “collects” payment data; the necessary data (IBAN, amount) is simply exposed to the customer.

The actual payment process only takes place on the customer’s smartphone: a SEPA transfer is executed in the customer’s banking app using the merchant’s IBAN.

Of course, this simple credit transfer option has existed for a long time, but from 2025, every account holder in the 20 eurozone countries must be able to make an “instant” credit transfer. The merchant receives his money in his account within seconds, making SCT Inst suitable for payment transactions at the POS.

Photo transfer via QR code and SEPA Instant Payment

The easiest way to transfer the IBAN and the payment amount from the merchant to the customer’s smartphone is a QR code. All mobile banking apps of the relevant banks offer the photo transfer function, which turns the QR code into a template for an (instant) credit transfer. In addition to the IBAN and the amount, each transaction should contain a clear purpose (account reconciliation for the merchant).

The buyer simply photographs the QR code in their banking app and authorises the transfer, e.g. using fingerprint or Face ID. They do not need to have NFC or Bluetooth activated.

In contrast to other payment methods, the customer does not transmit their payment details, but only receives the details for the transfer from the merchant. Fraudsters have no starting point for attacks and no expensive card terminal is required.

In accordance with SEPA regulations, the merchant receives a message from his bank about the incoming SCT Inst transaction within seconds.

Clearing and Settlement via TARGET

The core of a (credit) card solution is its own clearing and settlement system, in which the participants (cardholders and acceptance points) have accounts and the transactions are settled. The card organisations are largely owned by banks and must operate on a profit-oriented basis, and the fees are correspondingly high.

When SCT Inst is used at the POS, the market infrastructure of the European Central Bank (ECB) is used for clearing and settlement (TARGET). The ECB is an EU institution and is not profit-orientated. Although banks can charge a transaction fee for SEPA Instant payments, from 2025 this fee may not be higher than that of a conventional credit transfer.

The fee mechanisms of the card industry, such as the so-called interchange fee, do not exist in this system. Transaction processing is therefore dramatically more favourable for the acceptance point due to the system.

The Advantages of SCT Inst at the POS at a Glance

- minimal costs for the point of acceptance (just pay booking items at your own bank)

- no contracts or regulations – can be used by any SEPA account holder

- no card terminal, no open banking provider

- +340 million potential users

- Simple money transfer also between private customers (peer to peer)

- no foreign intermediaries (data security, EU sovereignty)

- no chargebacks

- no amount limit

Conclusion

The only hurdle to the widespread use of SCT Inst at the POS is still the lack of awareness among most account holders in the Euro countries. Although most of them already have their banking app on their smartphone, only around 20% currently use the photo transfer function.

Banks will not see the change in a positive light, as their earning potential is higher with card solutions (interchange fee). The greater loyalty of their account holders to the account is probably of little comfort to them.

As soon as the critical mass of users is exceeded, SCT Inst at the POS has the potential to make a significant contribution to cashless payment transactions in the Eurozone. The low costs, no amount limit and ease of use make SCT Inst at POS an outstanding payment system worldwide and relieve the economy in the Euro countries.

If you are a merchant, financial institution or operator of payment solutions and need support in implementing SCT Inst at the POS, we look forward to hearing from you.

Share

Weitere Artikel